New home sales in the GTA hit a record low in July, with only 654 units sold—a 48% drop from last year and 70% below the 10-year average. The market’s downturn is driven by rising inventory levels, now at 15 months, due to sluggish sales and a lack of new project launches. The ongoing high-interest rates have kept buyers on the sidelines, leading to stalled construction and a growing imbalance between supply and demand.

The new construction market’s weakness is evident in both condo and single-family home sales, with condo sales plunging 67% year-over-year and 81% below the 10-year average. Single-family home sales fared slightly better but were still 42% below the decade average.

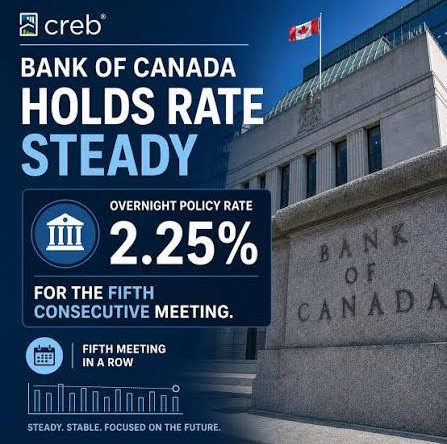

Given the state of the market, there are an almost unprecedented amount of buying opportunities. There is a lot of supply and many good options for those looking to break into the market. The Bank of Canada has also started lowering interest rates, with further cuts expected, which will likely boost activity meaning the lower-than-usual prices likely won’t last for too long.