The federal government hopes to make home ownership more accessible to first-time buyers with new mortgage rules that took effect Dec. 15.

Originally announced in September, the new rules enacted by the federal finance ministry aim to boost affordability for first-time millennial and generation Z buyers.

Here are some key points.

New price cap aims to boost affordability

As of Dec. 15, the federal government has raised the price cap for insured mortgages to $1.5 million from $1 million.

Canadian homebuyers offering a down payment of less than 20 per cent of the home purchase price must buy mortgage default insurance.

Until recently, properties costing $1 million or more weren’t eligible for insurance coverage. Recent changes mean more homebuyers can potentially qualify for a mortgage with a down payment of less than 20 per cent.

For example, the federal finance ministry said a minimum down payment on a $1.4-million home would now be up to $165,000 lower.

“This is helping more Canadians, especially younger generations, get those first keys of their own,” the ministry said in a Dec. 15 news release.

Expanded access to 30-year mortgages

Also in effect as of Dec. 15, the federal government is expanding the eligibility for mortgages at 30-year amortizations for first-time homebuyers and all buyers of new builds, including condominiums. First-time homebuyers can also access 30-year mortgage amortization on a new or resale property.

Mortgage amortization (the number of years it takes to fully repay a mortgage) are typically 25 years.

A 30-year option allows homebuyers to stretch the repayment period and reduce monthly payments. Previously, homebuyers with a down payment of less than 20 per cent were required to accept 25-year amortization.

The finance ministry said the new measures build on the Canadian Mortgage Charter, which allows all insured mortgage holders to switch lenders at renewal without being subjected to another mortgage stress test.

Mortgage stress test changes

Since 2018, Canadian homebuyers have been regulated by a mortgage stress that determines whether the borrower can handle a potential increase in their mortgage interest rate. To pass the test, purchasers must prove they can afford a mortgage at a qualifying rate higher than what their lender has approved.

Under new guidelines, if a homeowner with an uninsured mortgage is switching to a new lender and keeping the same amortization and loan amounts, the new lender won’t be required to apply a new stress test. This is also known as a straight switch.

Monthly savings

Back in September, mortgage broker Tracy Valko estimated that based on an average home price of $649,100, a 30-year amortization would reduce monthly payments by roughly $300 compared to a 25-year term based on current five-year mortgage rates.

But Valko suggested more changes are needed to boost affordability.

“This is not going to save our housing market!” Valko wrote in a post on X.

Canadians who opt for 30-year amortization will, of course, end up paying more in interest over the long run versus a 25-year mortgage.

A study by Canadian real estate website zoocasa.com in May suggested the monthly payment on a Greater Toronto Area home sold for about $1.11 million would be $6,344 based on a 25-year amortization, or $5,804 monthly at 30 years. Over the course of the loan, the borrower would pay $789,682 in interest over 25 years, compared to $975,945 over 30 years.

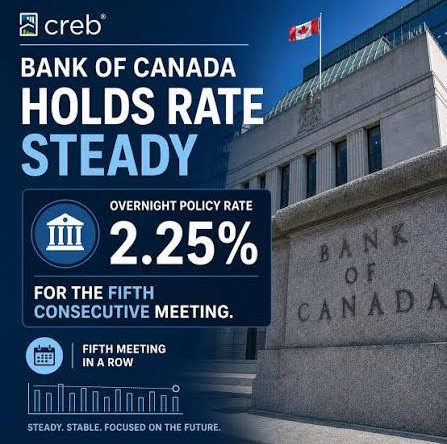

Lending rates lowered

Homebuyers should also remember that as of Dec. 11, the Bank of Canada has cut its overnight lending rate for the fifth consecutive time, dropping it to 3.25 per cent, the lowest it has been since September 2022.

Penelope Graham, ratehub.ca mortgage expert, said due to the rate cut, the prime lending rate will fall to 5.45 per cent and variable mortgage rates will also lower.

“If you currently have a variable rate mortgage, you’ll either see your payment lowered or more of your payment going toward your principal balance rather than servicing interest costs,” Graham said in a Dec. 11 update.

For example, the average variable borrower will see their monthly payment lowered by $180 based on a 10 per cent down payment on an average priced home of $696,166, with a five-year variable rate of 4.35 per cent, amortized over 25 years